In article 2 of our ongoing insurance series, Eric Veron and Ian Wittkopp discuss the impact that changing #technology and consumer tastes have on personal insurance lines. We describe how innovative insurtechs like #Lemonade, #Alan, and #ZhongAn are forcing incumbent insurers to adopt more customer-centric models and show where the future focus of innovation in personal lines may be.

Find article 1 here

When is the last time you bought travel insurance through a physical channel?

Personal insurance lines have been deeply impacted by two trends: improvements in technology (at a marginal cost) and changing customer expectations. Insurtechs have been amongst the first to adapt to these trends and have pushed incumbent insurers to innovate and transform in order to meet the expectations of changing customers.

These ‘innovation pressures’ are not equally exerted across all product categories – the complexity and purchase ‘trigger’ of some products limit pressures, such as with Life products. Furthermore, the pressures are not consistent in their solutions. Customers in P&C may demand an end to end digital experience, while in Health they may value a connected ecosystem of wearables and health care providers.

This article will offer an overview of how and why insurers should innovate in the personal insurance line space.

The innovation ‘landscape’ in personal lines

Personal insurance lines have been the first to experience pressure from changing technology and customer tastes. There are a few reasons for this. For example:

- Personal lines, especially simple P&C products like home and renters insurance, have a lower complexity than commercial insurance products. Lower complexity has created an easy entry point for insurtechs entering the space.

- Purchase drivers of personal products, or the ‘golden moment’ when insurance comes to the top of your mind, are more personal and customizable. For P&C products, these drivers are often consumption based.

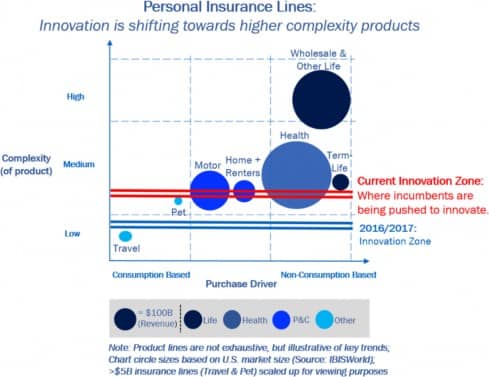

The table below examines the personal insurance lines which are facing pressure to innovate. We depict four categories: Life, Health, P&C, and Other, while ‘breaking out’ products within each category that are more susceptible to innovation (like Term-Life products within the larger Life Products category).

The ‘Current Innovation Zone’ depicts our opinion on where each insurance segment is in its innovation journey. For example, the personal motor insurance segment has nearly reached the halfway point of its innovation journey with InsurTechs like Roots and Metromile, and early adopter insurers like Progressive, spurring telematic/IoT adoption and adaptive pricing models throughout the industry. Among the top 10 Motor insurers in key markets, many have telematics/IoT programs or have piloted them.

In the following section, we’ll take a look at the key themes highlighted by the chart above.

Themes in personal insurance line innovation

Consumption-based, low complexity, products are the first to be disrupted

- When do you buy travel insurance? You are prompted to buy it when you check-out from a travel website. Travel insurance is the ultimate consumption based insurance product and as travel purchase channels changed (from agents to web/app and ecosystem tie-ups), insurance distribution models have also changed.

- Lemonade, which recently had a successful IPO, has been able to commoditize low complexity home & renters insurance (and now pet insurance) with an end.to-end digital model. In Q1 2020, Lemonade reached USD $133M in force premium, with roughly 730K customers, and a 147% growth rate from 2018 to 20191.

- Lemonade, and other insurtechs like Roots/Metromile, were the impetus for ‘all digital’ offering from incumbents like HiRoad, a wholly owned subsidiary of State Farm, that is focused on digital first auto insurance products. And of course, ZhongAn, a Chinese online-only P&C insurer, which is also leading the way in consumption-based insurance products. In 2019, ZhongAn increased GWP by 30% to RMB 14.6B (roughly USD $2B)2; the average premium of a ZhongAn policy was just USD $4, with cheap shipping return policies often costing less than RMB 1 (roughly USD $0.15). 3

Complexity limits innovation pressures for Life Insurance products

- Life products are more complex, and often bespoke, financial planning tools. Policy confirmation often requires medical check-ups and a high level of education is needed, even for the most astute consumers. Additionally, purchase triggers are focused on long-term financial planning which is an annual practice at most. Finally, with a ‘low touch’ product like Life insurance, it is hard to make the case, as an insurtech, that your process is differentiated and better.

- There are exceptions. Term-life products, duration focused coverage policies often used by younger consumers, are currently an area of intense innovation. HavenLife, by MassMutual, is a leading ‘digital first’ platform for these products. Another example is Blue, a virtual insurer in Hong Kong entering the life, savings, critical illness and personal accident cover segments. Finally, Singlife, a Singapore based digital life provider, which has begun to entice younger customers by offering a Singlife debit card that gives free life insurance coverage up to 5% of account value. This offering had 90K downloads in its first two months after release and is an onramp to higher complexity and higher margin life products for younger consumers.4

Innovation in Health Insurance is dependent on geography

- Health insurance programs differ greatly by country and thus complexity varies due to different regulations and market structure. In geographies with high standardization among certain (often government led) policies, insurtechs have been spurred to innovate. For example, Bowtie, a virtual insurer in Hong Kong, offers a basic product based on the government’s Voluntary Health Insurance (VHIS) program, Oscar in the United States offers basic Medicare plans, and Alan in France offers a basic health insurance plan to individual and companies.

- Although the proportion of premium underwritten by these insurtechs is relatively modest at this time, insurers have begun to react. However, innovation from these insurers has been slower than in P&C, likely because churn rates are lower too.

Innovation Pressures Differ Across Product Segments

- In P&C, customers want an end-to-end digital process with fast on boarding and even faster claims. Therefore speed, simplicity, price and claims resolution quality are the main drivers pushing innovation.

- While the end-to-end digital process is important in Health lines, customers also value an ecosystem that can provide them with wellness tips and customized health advice from their service providers. Personalised insights from wearables are also an important part of this experience.

- In Life, accessibility has long been an issue. Digital channels, like the one HavenLife is providing for term-life, are important, but internal digital capabilities are vital to improved cost structures and lower commission rates.

Implications for Insurers

Implications for insurers vary by product segment.

- In P&C, accessing and interacting with your customers differently is simply a must. Quick and automated on boarding is an industry standard, while automated claims pay-outs, virtual accident assessments, and adjustable rates based on sensors or telematics will be the new standard.

- While penetration from InsurTechs may be low, they have spurred innovation throughout the ecosystem and exposed incumbent’s high legacy cost structures that are high-touch and human driven, as unstainable and uncompetitive in the long term.

- Life products have thus far seen little disruption, owing in large part to complexity and social preference for human/agent distribution. We expect new channels that skew towards digital to be increasingly important. In many markets (mature and emerging), we have begun to see successful ‘e-bancassurance’ partnerships.

- As ‘robo advisors’ and other financial focused tech continues to emerge, consumer tastes will begin to change regarding digital purchases. Leading Life insurers should be looking at innovating within distribution, but also looking inward at cost and commission structures. Going forward, it will be hard to justify high commissions given the focus on transparency, unless you are offering perceived and differentiated trust-based advice, requiring a continuous uplift of intermediaries’ skills.

- For Health, it’s important to note that lasting disruption often comes from start.ups that focus on underserved or ‘unprofitable’ customer segments. Building digital products around low-complexity government insurance schemes may not be profitable now, but it presents an attack vector that flexible and low cost insurtechs can use to challenge incumbents for higher price (and higher margin) policies.

Future Pieces

In future pieces, we will provide our viewpoint on the following questions:

- Which business insurance segments is innovation pressuring?

- What technologies are at the forefront of insurance innovation?

- Where do insurtechs fit into the insurance value chain?

- Do insurtechs have enough differentiation to sustain a competitive advantage?

- What should incumbent insurers do to respond?

Sources

- Lemonade S-1 Filing (pg. 86, 91, 103), SEC – Edgar Database, June 2020.

- ZhongAn Online Pursuing High Quality Growth, 2019 GWP Up 30%, Markets Insider, March 2020.

- Oddball Policies Give Boost to China’s Insurers, The Wall Street Journal, September 2019.

- Singlife shows traditional insurers how to thrive in the new normal, Insurance Asia, June 2020.